Table of Contents

TLDR: Payment gateway integration is not a plug-and-play task. Your architecture choice, hosted fields vs direct API, determines your PCI scope, fraud exposure, and transaction cost before you write a single line of code. Most teams pick the gateway first and pay for that order of operations later.

The decisions you make during payment gateway integration affect your application's security, compliance, scalability, and long-term maintenance. Selection of the wrong approach early can lead to unnecessary complexity, higher costs, and expensive rebuilds later.

The right process is simple: define your payment architecture first, select the gateway that fits your business model, and then evaluate security, compliance, and pricing considerations. Following this sequence helps you avoid costly mistakes and build a payment system that scales with your business.

Whether you are launching a SaaS platform, marketplace, subscription service, or e-commerce store, this guide on payment gateway integration will help you understand the key architectural decisions, compare leading payment gateways, and choose the best solution for your specific requirements.

A payment gateway is the data transmission layer between your checkout and the payment network. It encrypts card data, passes it to the processor, and returns an approval or decline.

A payment gateway integration is not responsible for holding funds, underwriting risk, or serving as your merchant account. It simply facilitates the secure authorisation and transmission of payment data.

| Entity | Role | Examples |

| Gateway | Encrypts and routes transaction data | Stripe, Razorpay, Braintree |

| Processor | Moves money between banks | TSYS, Worldpay |

| Acquirer | Holds your merchant account | Chase Paymentech, Fiserv |

| PayFac | Bundles all four under one contract | Stripe, Square |

Most modern payment gateway integration setups use a PayFac model, where Stripe or Square acts as all four entities. This simplifies onboarding but limits negotiating power at scale.

Using a PayFac like Stripe enables faster setup and lower compliance overhead, but account suspension and risk decisions remain under the provider's control in integrate payment gateway.

A direct merchant account through an acquirer gives you more control, more negotiation room on pricing, and harder integration work. If your monthly volume exceeds $500,000, the direct route almost always wins on cost.

The payment gateway integration architecture you choose is not a frontend decision. It is a compliance, conversion, and engineering decision that affects every layer of your stack.'

No payment gateway is universally best. The right payment gateway integration choice depends on four axes, and most teams shortcut this analysis and regret it.

Stripe covers 46 countries with local acquiring in most. Razorpay covers India with UPI, NetBanking, and BNPL built in. Adyen covers 200+ markets with local payment methods.

If your users are in India, integrate payment gateway through Razorpay first. If they are in the US and EU, Stripe. If they span Southeast Asia or LATAM, Adyen or a regional gateway wins.

| Model | Best Gateway | Reason |

| Subscription | Stripe, Chargebee with Stripe | Native recurring billing setup |

| Marketplace | Stripe Connect, Adyen Platforms | Split payments, KYC, payouts |

| One-time e-commerce | Razorpay, Stripe, Square | Simple checkout, fast setup |

| In-person with online | Square, Stripe Terminal | Unified hardware and API |

Flat-rate pricing (Stripe at 2.9% + $0.30) is convenient below $50K monthly volume. Above that, interchange-plus pricing saves 20 to 40 basis points per transaction.

At $1M monthly volume, that is $2,000 to $4,000 per month in unnecessary fees. Negotiate before you scale, not after, in payment gateway integration.

Every major integrate payment gateway provides SDKs for popular programming languages. What separates them is the quality of their developer experience, documentation, and payment API integration resources.

Stripe leads in documentation depth, Razorpay supports a broad range of web and mobile frameworks, and Braintree offers stable SDKs with a steeper learning curve.

Each gateway has a different integration complexity, compliance posture, and commercial model. Here is what actually matters for your payment gateway integration decision.

Stripe's API is the benchmark. Webhooks, idempotency keys, and test mode are all first-class. Stripe's documentation covers nearly every payment gateway integration scenario, from basic setups to advanced use cases.

Best For: SaaS, marketplaces, US/EU consumer products.

Pricing: 2.9% + $0.30 per transaction (flat-rate), interchange-plus available at volume

Razorpay is a strong payment gateway integration choice for India-first products, with UPI and NetBanking available as native payment methods rather than add-ons.

Key Features:

Best For: India-first products, D2C, edtech, fintech.

Pricing: 2% per transaction for most methods.

If PayPal adoption is important to your customer base, Braintree is the most direct integration path for payment gateway integration.

It combines traditional card processing with access to PayPal's global wallet ecosystem, helping improve conversion rates among international buyers and users who prefer digital wallets.

Key Features:

Best For: Subscription businesses, SaaS platforms, marketplaces, and merchants with significant PayPal usage in payment API integration.

Pricing: Standard card processing fees vary by region, with PayPal transaction fees applied where relevant.

Square is designed primarily for businesses that combine physical and online sales.

Its POS ecosystem is one of the strongest in the market, but its payment gateway integration capabilities are less flexible than Stripe's.

Key Features:

Best For: Retail stores, restaurants, service businesses, and omnichannel merchants.

Pricing: Typically starts around 2.6% + $0.10 for in-person transactions, with separate pricing for online payments in payment gateway integration.

Adyen is built for large-scale businesses that need a single payment infrastructure across regions, channels, and currencies.

Its payment gateway integration capabilities support global acquiring and unified commerce, making it a popular choice of payment API integration for enterprise organisations.

Key Features:

Best For: Enterprises, global brands, marketplaces, and businesses processing high annual transaction volumes.

Pricing: Interchange++ pricing model with additional processing fees. Typically most cost-effective at enterprise scale rather than for startups or small businesses.

A production payment gateway integration is not just a charge call. It is a five-phase, step-by-step integration process where each phase has failure modes the next phase cannot fix.

Separate API keys per environment. Never hardcode keys in source code for payment gateway integration. Use environment variables and a secrets manager (AWS Secrets Manager, HashiCorp Vault). Rotate keys quarterly.

Use hosted fields for all card input. Render Stripe Elements, or Braintree hosted fields inside iframes. Your JavaScript should never read raw card values. Pass only the payment token to your backend for payment gateway integration.

Create the Payment Intent server-side with the amount, currency, and customer ID. Never create charges from the frontend. Validate order totals server-side before every charge call. Payment gateway integration charge logic with idempotency keys on every request.

For secure payment API integration, register webhook endpoints for payment_intent.succeeded, payment_intent.payment_failed, and charge.dispute.created at minimum. Verify webhook signatures on every received event. Return 200 immediately and process asynchronously.

Test declined cards, insufficient funds, 3DS2 authentication, and network timeouts. Stripe and Razorpay both provide specific test card numbers for each failure mode. Sandbox success does not guarantee production success in edge cases on payment gateway integration.

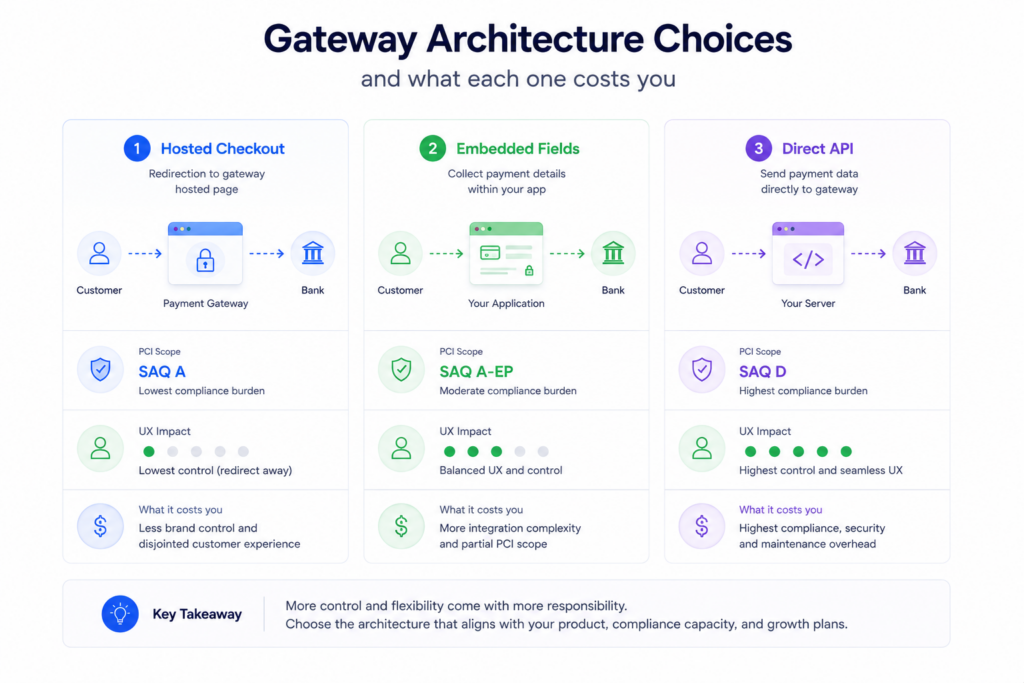

Your payment gateway integration architecture directly impacts PCI DSS compliance. It determines your compliance scope, the SAQ category you qualify for, and the security controls your organisation must maintain for payment API integration.

| SAQ Type | Controls | Typical Use Case |

| SAQ A | 22 | Fully hosted payment page or redirect where card data is handled entirely by the payment provider |

| SAQ A-EP | 61 | Hosted fields or embedded payment components on merchant-controlled pages |

| SAQ D | 329 | Direct API integrations where merchant systems handle cardholder data |

Webhook reliability is the backbone of any payment gateway integration. Production systems fail silently here while sandbox tests pass perfectly.

Sandbox webhooks deliver instantly to localhost via tunnels. Production webhooks hit real servers with real load, timeouts, and deploy windows.

The most common production failures: server returning 500 during a deploy, database deadlock on duplicate event processing, and missing signature verification causing dropped events.

A payment gateway integration is only as effective as its fraud controls. Relying solely on default settings can lead to unnecessary declines or missed fraud risks as your business grows.

Gateways do not guarantee event order. A charge. succeeded event can arrive before payment_intent.created in high-load scenarios.

Design your payment API integration webhook handlers to be stateless relative to event order. Process each event based on its own payload, not assumed prior state.

Default fraud settings within a payment gateway integration are built for typical merchant behaviour. Businesses with unique transaction patterns may need custom rules to prevent false declines and improve fraud detection.

Stripe Radar's default ML model is a starting point.

Build custom rules for your transaction profile: block cards from high-risk BINs in your vertical, flag orders where billing and shipping ZIP codes do not match, and require 3DS2 for orders above your average order value.

The posted rate is not your effective rate. Every payment gateway integration has a total cost of ownership that the pricing page does not show you.

| Model | Best For | Cost at $100K Volume |

| Flat-rate (2.9% with $0.30) | Early-stage businesses, under $50K/month | ~$2,900 |

| Interchange-plus (0.2% with interchange) | Growing businesses, $50K+/month | ~$1,800 to $2,200 |

| Blended custom pricing | Enterprise businesses, $1M+/month | Negotiated |

Processing fees are only part of the total cost of a payment gateway integration. Chargeback fees ($15 to $25 per dispute), international card surcharges (up to 1.5%), currency conversion fees (1 to 2%), and monthly account fees can significantly increase your actual payment costs. Many teams discover these expenses of integrate payment gateway only after their payment API integration is already live.

To compare gateways accurately, look beyond the transaction rate. Include processing fees, chargeback costs, fraud prevention expenses, and the engineering effort required to maintain the integration.

For instance, a payment gateway integration that charges 0.3% more per transaction may still be the better choice if it reduces fraud and chargebacks enough to lower overall costs. Evaluating the complete cost picture before selecting an integrate payment gateway can save substantial money as transaction volume grows.

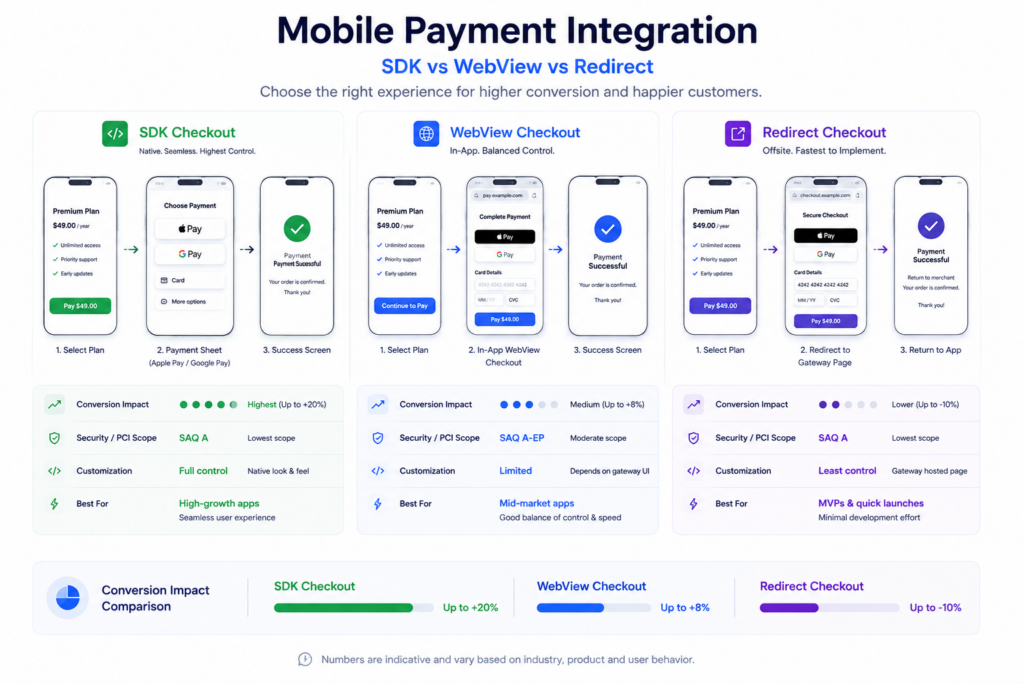

Mobile payment integration typically follows one of three approaches. Each offers different trade-offs in conversion rates, PCI compliance scope, and implementation effort.

| Approach | Conversion | PCI Scope | Effort |

| Native SDK | Highest | SAQ A / SAQ A-EP | High |

| Embedded Checkout | Medium | SAQ A-EP | Medium |

| Redirect | Lowest | SAQ A | Low |

A single-gateway setup creates a single point of failure, which is why gateway failover and redundancy planning matters. Every production-grade payment gateway integration should include a failover strategy to reduce revenue loss during outages, network disruptions, or processing delays.

No payment API integration can guarantee 100% uptime for integrate payment gateway. Even a short outage can impact revenue and customer experience. When evaluating providers, look beyond SLA promises and review their incident history, transaction success rates, status page transparency, and recovery processes in payment gateway integration.

For high-volume payment gateway integration environments, use a primary gateway and automatically fail over to a secondary provider when gateway errors or outages occur. Do not retry issuer-declined transactions, and maintain routing logs for auditing and reconciliation. This approach improves reliability and creates a more resilient integrate payment gateway architecture.

Use this before you integrate payment gateway into any production system. Each point maps to a real failure mode.

1. Geographic coverage matches your primary markets. Confirm local acquiring, not just currency support. Local acquiring reduces decline rates by 10 to 15% versus cross-border processing.

2. Published or negotiable pricing with no mandatory blended tiers. Blended pricing hides your effective rate. Require line-item fee disclosure before signing.

3. Hosted fields or SDK available for your frontend stack. Verify compatibility with your framework before committing to a payment gateway integration.

4. Webhook delivery with documented retry policy and signature verification. No retry policy documentation is a red flag for production reliability.

5. Idempotency key support on charge creation. Non-negotiable for any payment API integration handling retries.

6. 3DS2 support for your target markets. Mandatory for EU transactions under PSD2. Required for reducing liability on disputes.

7. SLA equal to or above 99.99% with status page and incident history. Review the last 12 months of incidents, not just the published SLA.

8. Fraud tooling with configurable rule sets. Default rules are insufficient for non-standard business models.

9. PCI DSS Level 1 certification. Any integrate payment gateway vendor without Level 1 certification is a compliance risk.

10. Account termination policy is documented, and appealable PayFac models have broad termination rights. Read this clause before you build on the platform.

Payment gateway integration done right means your architecture, compliance posture, and fraud configuration are all decided before the first line of code is written. Patoliya Infotech builds payment gateway integration systems that are designed for production from day one, not retrofitted after launch.

What this means for your product:

Patoliya Infotech's team has built integrate payment gateway systems for SaaS, marketplaces, and D2C products across India, the US, and EU markets. If your team is deciding between architectures or gateways, let's map out the right stack for your volume and market before you commit.

Payment gateway integration is not a feature. It is infrastructure. Your architecture choice sets your PCI scope. Your gateway choice sets your cost at scale. Your webhook and fraud configuration sets your operational resilience. Get the sequence wrong, and you rebuild, not patch. The framework in this guide architecture first, gateway fit second, compliance and cost third, is the order that works in payment API integration. If you are ready to scope the right payment gateway integration for your product, let's talk.