Table of Contents

Shopify now earns more from financial products than from software subscriptions. Toast processes billions in restaurant payments annually. These are not fintech companies. They are SaaS businesses that understood one thing early: the most defensible revenue a platform can generate flows through the product, not around it.

That shift is what embedded finance makes possible, and it is why this guide exists. By the time you finish reading, you will have a complete decision framework covering product tiers, vendor selection, ROI modeling, and the compliance realities most guides deliberately skip.

Embedded finance is the integration of financial products directly into a non-financial software platform. Payments, lending, accounts, cards, insurance, or investment capabilities live inside your workflow, branded as yours, powered by licensed infrastructure underneath. The user never leaves your product to access a financial service. That native experience is the entire point.

A link to a third-party bank is not embedded finance. A payment button that routes through your platform, settles into a wallet you manage, and generates per-transaction revenue is. The distinction determines whether you capture the economics or hand them to a competitor.

These three terms appear interchangeably in vendor marketing. They describe three distinct layers of the same stack.

The term became commercially toxic after the Synapse collapse in 2024. That failure left millions in end-user funds trapped in a reconciliation gap between fintech middleware and sponsor banks. Vendors now prefer "embedded finance infrastructure" or "banking API." The underlying services are identical. The regulatory scrutiny is materially higher, and sponsor banks that remain in the market are significantly more selective about platform partners. The language changed because the risk profile changed.

Every embedded finance product falls into one of five tiers. Not every tier carries the same implementation weight or compliance exposure, and choosing the wrong starting point is one of the most common reasons embedded finance projects run over time and budget. Here is how the tiers stack from fastest path to production to longest runway.

Embedded Payments Payment processing, split settlements, and marketplace payouts is where almost every platform should start. The API surface is well-documented, the compliance overhead is manageable, and the time from sandbox to production is measured in weeks rather than months. The revenue model is a transaction markup, typically 15 to 50 basis points on gross payment volume.

Stripe Connect, Adyen for Platforms, and Payoneer are the dominant infrastructure providers here. Whether to add embedded payments is no longer the question in most B2B SaaS verticals; it is table stakes. The real question is whether your current implementation is capturing the revenue you are entitled to.

Embedded Lending and Working Capital revenue-based advances, invoice financing, and B2B BNPL sit at the second tier of complexity. The data a SaaS platform already holds, transaction history, revenue trends, customer tenure, is exactly the underwriting signal that makes embedded lending economics work. You are not a credit company guessing at risk. You already know these businesses.

Compliance exposure increases materially here. Lending origination requires either a licensed lending partner or your own license in some geographies. The bank carries the credit risk, but your platform owns the relationship and bears reputational exposure when loans underperform. Build this embedded finance product only when transaction volume creates defensible underwriting signal, typically above $1M in monthly GMV per cohort.

Embedded Banking issuing real deposit accounts, virtual or physical cards, and maintaining a customer ledger is where implementation timelines extend to 9 to 15 months and compliance requirements become genuinely demanding. The bank's BSA/AML review process alone typically adds 3 to 6 months after contract signing.

The economics at scale are compelling. A platform managing float earns net interest income. A card issuer earns interchange. A ledger business earns on volume, float, and cross-sell. This is the tier that explains why Shopify Balance and Toast Capital exist.

Embedded insurance remains one of the most underbuilt product categories in vertical SaaS. Not because demand is weak but because distribution has historically been complex. Insurance carriers required volume commitments early-stage platforms could not meet, and the regulatory patchwork across US states adds compliance overhead most CTOs underestimate.

For vertical platforms with concentrated industry exposure, the opportunity is real. A construction management SaaS offering builder's risk coverage to its contractor base has a captive distribution channel no carrier can replicate. The technical lift is lighter than embedded banking. The regulatory and actuarial work is heavier. Partnerships with MGAs or platforms like Boost or Openly are the practical path for most SaaS builders today.

Investment products sit at the frontier of what platforms are deploying. Investment advisor registration, custody requirements, and FINRA oversight in the US create a regulatory burden that is substantial by any measure. For most B2B SaaS founders reading this, Tier 5 is a 2027 or 2028 roadmap item, not a current priority.

Embedded finance market size estimates range from $104 billion to $7 trillion depending on the report, the methodology, and who commissioned it. Both numbers are technically defensible and practically useless for a SaaS founder building a board-level business case.

The $7 trillion figure represents total financial services spend that could theoretically flow through non-financial platforms over a multi-decade horizon. The $104 billion figure represents platform revenue specifically attributable to financial product distribution by 2030. Neither figure tells you what your addressable opportunity actually is. [LINK OPPORTUNITY: McKinsey embedded finance market size report]

The number that matters is the financial transaction volume your customers currently conduct outside your platform. That is the revenue you are leaving with a competitor or a bank. Quantifying that single figure is the first analytical step in any serious embedded finance business case.

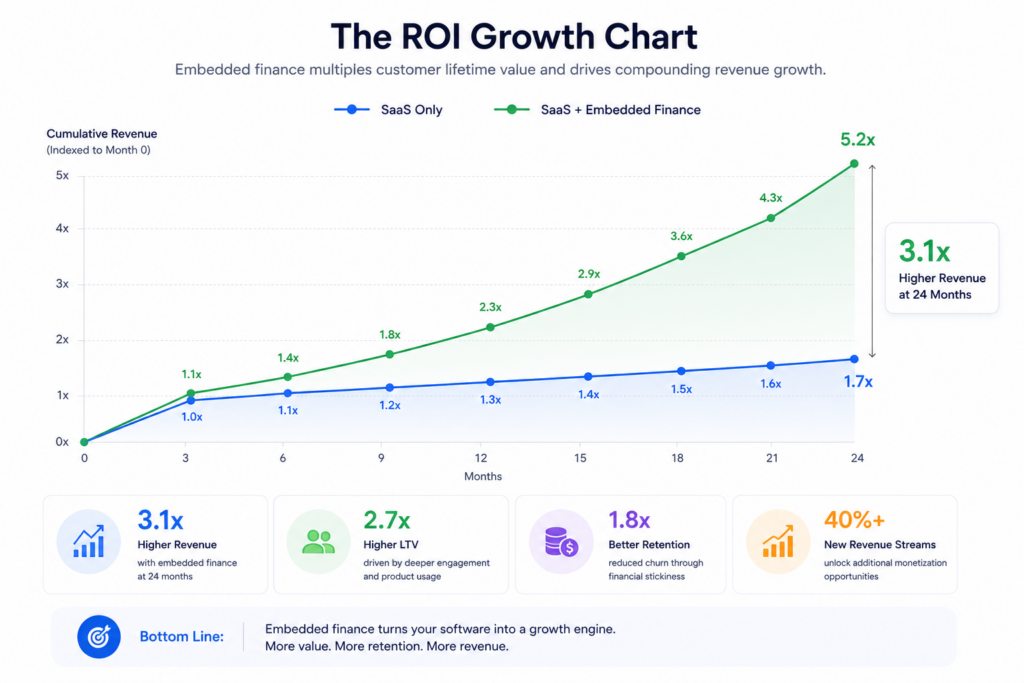

McKinsey research shows platforms with integrated financial products generate 2 to 5 times higher customer lifetime value and 30% lower customer acquisition cost than platforms offering software alone. [LINK OPPORTUNITY: McKinsey "Embedded Finance: Who Will Lead the Next Payments Revolution?"] Joint research from Adyen and SaaStr indicates platforms with strong financial product adoption generate up to 70% more revenue per customer than software-only comparables.

The mechanism is not complicated. Financial product usage creates daily active engagement that software dashboards rarely achieve. A business owner checks their embedded account balance more often than they open a reporting module. That daily touchpoint is the structural advantage that makes integrated financial product economics so durable once adoption reaches 20 to 30% of the user base.

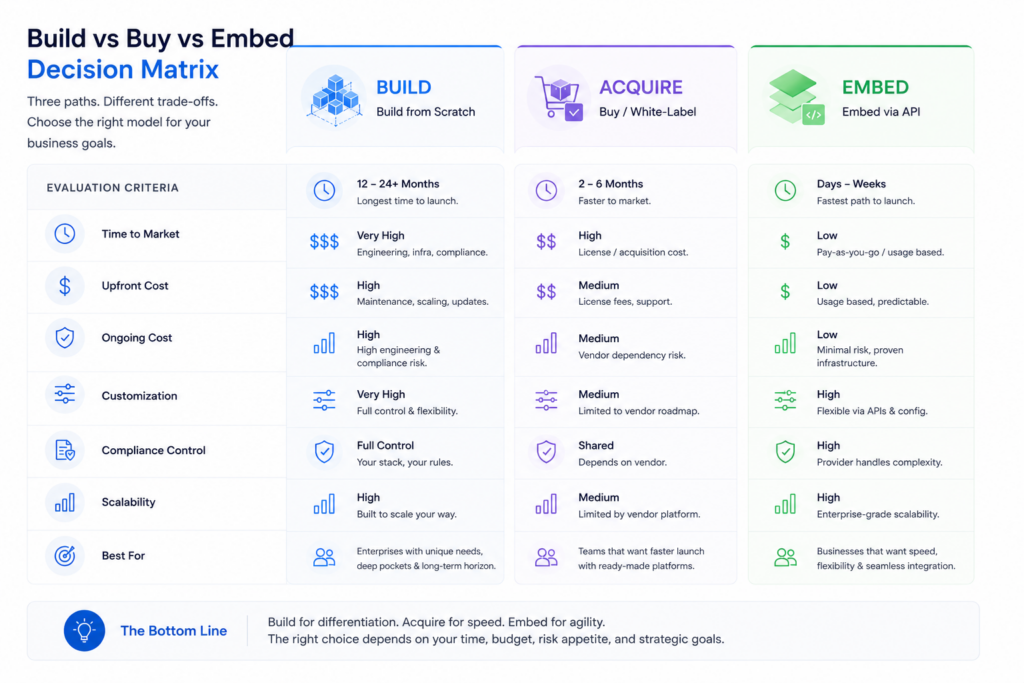

Three paths exist for any SaaS platform entering embedded finance. Most platforms at early or mid-stage have exactly one real option, but the table below lets you verify that for your specific situation across all the dimensions that actually matter.

| Build from Scratch | Acquire a Fintech | Embed via BaaS Provider | |

| Time to market | 3 to 5 years | 12 to 24 months | 3 to 15 months |

| Capital required | $10M+ minimum | $5M to $50M+ | $50K to $500K |

| Compliance ownership | Fully yours | Inherited; audit required | You own BSA/AML; provider holds the license |

| Biggest risk | Runway burns before launch | Compliance and technical debt arrive with the deal | Sponsor bank concentration; vendor lock-in |

| Embed now if | — | — | $500K+ monthly GMV, a competitor has launched, or your workflow already touches the transaction |

| Wait if | — | — | ARR below $3M, compliance budget is zero, or customers span geographies no single BaaS provider covers |

| Geography fit | Any, if you can fund it | Any, with the right target | US: deepest ecosystem. UK: FCA clarity, direct-licensed banks. EU/EEA: PSD2 and open banking advantage. Multi-geo: Airwallex is the clearest option |

| Right for | Platforms projecting $100M+ financial product ARR within 5 years | Platforms with M&A infrastructure and a specific fintech gap to fill | 95% of SaaS businesses evaluating embedded finance today |

Understanding embedded finance pricing before you enter a vendor conversation is one of the few negotiating advantages a platform has. Most vendors anchor on the headline rate and bury the real cost structure in the contract. Here are the four models in use and the hidden line items that follow each one.

Revenue share and transaction markup is the most common model in Tier 1 and Tier 2 implementations. The vendor takes 10 to 40 basis points on transaction volume processed through their infrastructure. Your margin sits on top. Revenue share alignment is strong at scale; unit economics are thin early when volume is low.

Monthly platform fee plus per-API-call pricing is common in banking API providers and infrastructure-oriented vendors. It creates predictable base cost and variable cost that scales with usage. The trap is per-API-call fees on reconciliation and compliance calls, which can compound in ways the initial contract does not make obvious.

Volume-tiered enterprise licensing is typical for Tier 3 and Tier 4 implementations where the vendor carries more compliance responsibility. Annual contracts with minimum volume commitments and tiered rates above thresholds. Negotiate the volume minimums carefully; missing them in year one is common for platforms that overestimate early adoption speed.

Setup and integration fee plus SaaS subscription is the model used by compliance-first providers who want revenue independent of your transaction volume. Lower vendor risk, higher upfront cost for you.

The line items that do not appear in any vendor's pricing deck:

BSA/AML program development runs $50,000 to $200,000 in legal and compliance consulting fees before your first embedded finance production transaction. This is a regulatory requirement, not optional.

KYC vendor costs add $0.50 to $3.00 per onboarded business depending on verification depth. At 5,000 users that is $2,500 to $15,000 in one-time cost plus ongoing re-verification cycles.

Automated compliance monitoring is not sustainable as a manual process past $5M in monthly volume. Budget $2,000 to $15,000 monthly for a dedicated tool.

Ongoing compliance staffing means a compliance officer or fractional compliance management firm as a permanent operating cost once live. Budget $80,000 to $150,000 annually fully loaded.

Migration and exit costs exist in almost every contract as theoretical data portability provisions that are practically expensive to exercise. Negotiate explicit migration assistance terms before signing, not during a vendor transition.

The model that holds up in a board presentation:

Incremental Annual Revenue = Active Users x Adoption Rate x Average Revenue Per Adopted User

For a platform with 5,000 active business users: conservative adoption at 20% yields 1,000 users. Average revenue per adopted user from payments, float, and interchange: $500 to $1,500 annually. Incremental revenue range: $500,000 to $1,500,000. Against an implementation cost of $100,000 to $300,000 and a 24-month ramp, the IRR on a conservative scenario lands between 40% and 120%.

Shopify's financial solutions segment consistently generates gross profit that exceeds its SaaS subscription gross profit. Toast Capital has advanced hundreds of millions in working capital to restaurant customers, directly reducing churn by increasing switching cost. McKinsey's SaaS embedded finance benchmark shows 2 to 5x LTV improvement at adoption rates above 30%. Adyen and SaaStr joint data shows platforms with embedded payments earn up to 70% more per customer than software-only comparables.

These are not projections. They are outcomes from platforms that moved 3 to 5 years ago. The benchmark gap between early movers and platforms moving now is real but not insurmountable, provided implementation is executed correctly.

Adoption below 15%. If fewer than 1 in 6 customers activates the financial product, fixed compliance and operational costs will not be covered by transaction economics for several years. Low adoption is almost always a product-fit problem, not a marketing problem.

Sponsor bank regulatory action. If the partner bank receives a consent order or exits the market, your production environment can be suspended with 30 to 90 days notice. This is not theoretical. It has happened to recognizable platform names. Diversified bank coverage is an operational requirement, not a nice-to-have.

Fraud loss exceeding interchange income. In the first 12 months of a card or account product, fraud rates can run 2 to 5 times higher than steady state. Immature fraud controls combined with thin interchange economics can produce net negative unit economics for the entire first year.

These three scenarios share a common cause: a business case built on adoption and revenue projections without equal rigor on the cost and risk side. The vendors who present you with compelling embedded finance financial models are not modeling your fraud loss at month three or your compliance staffing cost in year two. Stress-test every scenario with conservative assumptions before you take the proposal to your board.

In 2024, Synapse Financial Technologies, a middleware infrastructure provider serving dozens of embedded finance platforms, filed for bankruptcy. [LINK OPPORTUNITY: FDIC Synapse report or Bloomberg coverage] The resulting reconciliation failure left an estimated $65 to $96 million in end-user funds unaccounted for between Synapse's ledger, its sponsor banks, and its platform clients. Customers could not access their own money for months.

The failure was a ledger reconciliation failure compounded by ambiguous legal ownership of funds across the middleware and sponsor bank boundary. The lesson: the middleware layer you choose is a critical dependency in whether your customers can access their own money. Vendor financial stability, bank relationship transparency, and contractual fund segregation are not due diligence checkboxes. They are existential questions.

Regulatory and compliance risk is the exposure your platform bears when your BSA/AML program is incomplete, KYC procedures are inadequate, or transaction monitoring fails to catch suspicious activity. Enforcement actions come against the platform operator, not only the infrastructure provider. Build the compliance program first. Deploy the product second.

Fraud and identity risk in an embedded finance product is structurally different from application-layer fraud because it can produce direct financial loss. Mobile fraud in financial applications grew 7% year-over-year between 2024 and 2025. [INSERT STAT: source citation] Build fraud controls into the product specification, not as a post-launch retrofit.

Vendor lock-in risk is acute because customer financial data, ledger history, and account relationships are difficult to migrate. A vendor that controls your customers' account numbers effectively controls the relationship. Negotiate data portability and account number portability terms before any contract is signed.

Operational risk covers infrastructure uptime, API reliability, and incident response. Financial products operate under a fundamentally different uptime requirement than SaaS dashboards. A reporting tool going down for two hours is an inconvenience. A payment processing outage during payroll is a business crisis. Require SLA terms with financial penalties, not just "commercially reasonable efforts" language.

Before your first embedded finance API call in production, your platform needs a functioning BSA/AML program that includes: a written policy reviewed by qualified legal counsel, a KYC onboarding procedure with defined due diligence levels, a transaction monitoring protocol with defined escalation paths, a suspicious activity reporting (SAR) filing process, and a named compliance officer or third-party compliance management firm.

This is not the infrastructure provider's job to build for you. They supply the tools. You build the program. Legal and consulting cost to do it properly runs $50,000 to $200,000 depending on product complexity. Budget for it before the implementation project starts, not as a launch-week surprise.

The sequence that works: compliance program design in month one, KYC workflow build in month two, sandbox integration in parallel, and transaction monitoring live before a single production user is onboarded. Platforms that reverse this order, integrating first and building the compliance program under time pressure, spend two to three times as much fixing what they should have built correctly once. The compliance program is not a box to check. It is the foundation the product runs on.

Choosing the wrong embedded finance vendor is expensive in ways that extend well beyond the contract value. Switching costs are high, migration is painful, and the compliance program you built around one vendor's tooling does not transplant cleanly to another. Evaluate against all eight criteria before any demo.

Licensing posture: Does the vendor hold its own bank charter or EMI license, or does it rely on sponsor bank pass-through? Direct licensing means fewer intermediary failure points. Fintech middleware means faster setup but more counterparty risk.

Geography coverage: Does the vendor cover every market your customers operate in today and your likely expansion markets in the next 24 months? A US-only vendor is the right answer if your roadmap is US-only. It is a structural trap if EU or UK expansion is on the plan.

Bank network depth: How many banks does the vendor have in its network? Ask explicitly: if the primary sponsor bank exits the market, what is the continuity plan and realistic timeline?

Compliance tooling: Does the vendor offer transaction monitoring, KYC orchestration, and AML screening built in, or do you need to integrate those separately? Third-party compliance tools typically add 30 to 50% to the headline platform fee.

Sandbox fidelity: Can you complete a full payment or account lifecycle in sandbox before signing a production contract? A sandbox requiring manual overrides is a red flag for production readiness.

SLA and uptime: What is the contractual uptime commitment, how are downtime credits calculated, and what is the historical incident record? Request the last 12 months of incident logs, not just the SLA document.

Pricing and exit terms: Get the complete embedded finance fee schedule in writing including all API call types and volume penalties. Negotiate data portability and migration assistance terms before signing. Exit terms are established at contract, not at termination.

Implementation support: A dedicated integration engineer for the first 90 days is materially different from documentation and an async Slack channel. Clarify exactly what onboarding includes.

| Vendor | Geography | Licensing Model | Best For | Compliance Overhead | Notable Trade-Off |

| Stripe Treasury | US primary | Middleware (bank partners) | Stripe-ecosystem SaaS | Low (Stripe handles) | Not standalone outside Stripe Connect |

| Unit | US | Middleware + bank network | B2B SaaS, fintech startups | Medium | No direct bank license; monitor post-2025 regulatory posture |

| Marqeta | US, UK, EU | Card program manager | Card-first products, gig economy | Medium-High | Enterprise volume minimums; less suited for early-stage |

| Treasury Prime | US | Middleware + direct bank contracts | Platforms wanting bank relationship control | High (you own compliance) | Best pricing leverage; most compliance responsibility |

| Synctera | US | Middleware + community bank network | Compliance-first platform | Medium-High | Smaller bank balance sheets; strong BSA tooling |

| Airwallex | Global (80+ licenses) | Direct-licensed in multiple regions | Multi-country SaaS platforms | Low-Medium | Pricing opaque at mid-market volume |

| Griffin | UK | Direct-licensed bank | UK-based SaaS; regulatory clarity | Low (bank owns compliance) | UK only; waitlist for new partnerships |

| Swan | EU/EEA | Direct-licensed EMI (France) | EU SaaS needing IBAN accounts and data residency | Low | EU only; no US capability |

Early-stage US platforms under $5M ARR should evaluate Stripe Treasury first if already on Stripe Connect, and Unit as the primary alternative. Both offer faster sandbox access, lower volume minimums, and documentation quality that suits lean engineering teams.

Growth-stage US platforms between $5M and $50M ARR building embedded banking seriously should evaluate Synctera and Treasury Prime. The compliance overhead is higher but the bank relationship transparency and product depth justify it at this scale. Treasury Prime in particular offers strong pricing leverage for platforms willing to own more of the compliance program.

UK platforms where regulatory clarity is a primary concern should evaluate Griffin first. As a direct-licensed bank it eliminates the fintech middleware failure point entirely. Engage them early; the waitlist is real.

EU platforms with IBAN account or data residency requirements should evaluate Swan. The EMI licensing structure provides strong product coverage across EEA member states with a clean compliance posture. For multi-geography platforms, Airwallex is the clearest embedded finance option, though pricing transparency at mid-market volumes requires a direct commercial conversation rather than a public rate card.

The open API and account data infrastructure available in the EU and UK gives platforms in those markets a real underwriting and personalization advantage in lending and working capital products that US platforms currently cannot replicate at equivalent cost.

Patoliya Infotech builds the integration layer between your SaaS product and the underlying embedded finance infrastructure, not the infrastructure itself. That distinction matters because most of the implementation timeline is not API integration.

It is product design, compliance program architecture, KYC workflow development, ledger reconciliation logic, and the fraud controls that protect your customers from day one. The API integration is roughly a quarter of the total work. The compliance-ready product architecture is the other three quarters, and it is where embedded finance implementations most commonly run over time and budget.

A concrete example of what that looks like in practice: we built Alinea, a full AI-powered wealth management platform, over a two-year engagement. The scope covered personalized investment recommendations driven by user data and market signals, automated portfolio rebalancing that responds to changing market conditions, goal-based financial planning, real-time performance analytics, and a cloud infrastructure on AWS built for security and scale.

The technology stack ran Next.js on the frontend, Node.js and Express on the backend, MongoDB for the database layer, and AWS Lambda for serverless processing. Alinea sits squarely in Tier 5 of the product complexity stack described earlier in this guide, the most technically and regulatorily demanding category. It shipped. It scaled. It works in production.

That is the standard we bring to every embedded finance engagement regardless of product tier.

The embedded finance market in 2026 is no longer emerging. It is consolidating, and the SaaS platforms that moved first have built financial product revenue that structurally outpaces their software subscriptions. The platforms moving now face a more regulated environment and a more selective sponsor bank ecosystem, but they also have access to better tooling, clearer licensing frameworks, and post-Synapse compliance standards that the infrastructure providers take seriously.

The decision is binary: build embedded finance into your core workflow before your vertical competitor does, or cede that transaction layer to them permanently. The technical barrier is manageable. A capable CTO can evaluate and begin integrating a payments API in a quarter. The real obstacles are selecting the right vendor for your geography and stage, building the internal compliance program that sustains the product, and structuring the business case that gets the initiative properly funded. This guide gives you the framework for all three. The next step is the scoping call.